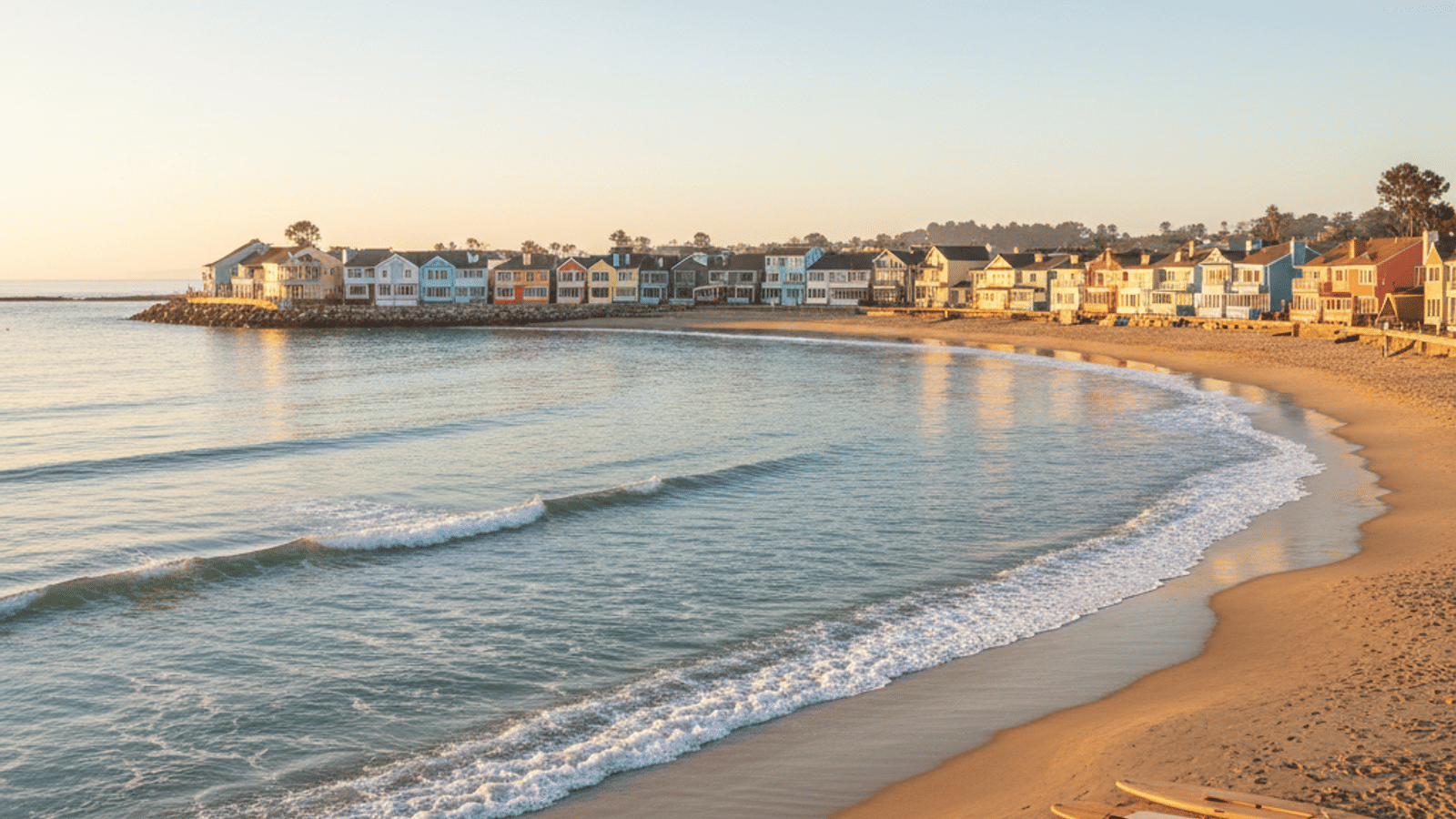

Let’s be honest right out of the gate: buying a home in Santa Cruz is a financial heavy lift. When you look at the sticker prices here compared to almost anywhere else in the country, it can feel discouraging. But then you look around at the redwood forests, the surf breaks at Steamer Lane, and the vibrant downtown culture, and you remember exactly why people fight to live here.

For first-time buyers, success in this market isn’t about finding a “steal”—those rarely exist here. It is about strategy. You need to understand the quirks of our local inventory, know which homebuyer assistance programs in Santa Cruz actually work (like Measure J), and have your financials polished to a shine.

The good news is that we are seeing a shift. Inventory levels have been creeping up, reaching heights we haven’t seen in six years. That gives you a little more breathing room than buyers had during the frantic pandemic years, but you still need to move smart.

The Santa Cruz Market: What First-Time Buyers Need to Know

Those who are transitioning from the rental market or relocating from Silicon Valley must quickly adjust their definition of an “entry-level” price point. While a starter home in other regions might cost $400,000, the Santa Cruz countywide median for a single-family home typically hovers between $1.3M and $1.36M, with prices in the City of Santa Cruz climbing closer to $1.7M due to coastal demand.

For many first-time buyers, this means the detached single-family dream may be a secondary goal; instead, condos in Live Oak or townhomes in Scotts Valley serve as essential stepping stones to stop paying a landlord’s mortgage and start building equity at a more manageable price.

Although the market has cooled since the 2021 frenzy, competition remains high for desirable homes priced under the $1.2M “sweet spot,” which often still attract multiple offers. However, current Santa Cruz housing market trends show a rise in active listings, offering buyers more breathing room than in previous years.

While you likely won’t have to make a decision within 15 minutes of a viewing, the environment still requires you to be financially prepared and ready to act decisively when the right opportunity appears.

Down Payment Assistance & First-Time Buyer Programs

This is where working with a local expert pays off. Many national lenders don’t know the ins and outs of our specific local affordability programs.

If you are struggling with the down payment or the monthly payment, these programs can be the difference between renting forever and getting your keys.

Measure J and Measure O

You can’t talk about affordable housing here without discussing the Measure J affordable housing program. This is a County initiative that requires developers to set aside about 15% of new units for moderate or lower-income buyers. These homes have price controls, meaning they are sold Below Market Rate (BMR).

To qualify, you generally need to meet income limits and, crucially, you must live or work in Santa Cruz County for at least 60 days prior to applying.

The City of Santa Cruz has a similar counterpart called Measure O. While the concepts are alike, the specific rules and qualifying developments differ because they fall under city jurisdiction rather than county. Both programs come with resale restrictions to keep the homes affordable for the next buyer, so they are great for stability but less focused on rapid equity growth.

State and Non-Profit Help

Beyond local measures, look into the CalHFA Dream For All program. This is a shared-appreciation loan from the state that can help with down payments, though demand is so high they have moved to a lottery system.

Locally, Habitat for Humanity Monterey Bay is another incredible resource. They offer up to $100,000 in down payment assistance for eligible buyers in the county who haven’t owned a home in the last three years. There is also the CalHome program, which offers deferred payment loans to help low-income households bridge the affordability gap.

Budgeting Beyond the Mortgage: Hidden Local Costs

The purchase price is just the headline number. To avoid surprises, you should factor these four specific local carrying costs into your monthly budget:

- Property Taxes: Budget approximately 1.1% of your purchase price annually to cover the base rate and local assessments.

- Closing Costs: Expect to pay between 2% and 3% of the purchase price for title insurance, escrow fees, and pre-paids.

- Fire Insurance: If buying in the redwoods or hills, you may need a California FAIR Plan policy, which can be significantly more expensive than standard coverage.

- HOA Fees: If you are targeting a condo or townhome, these fees factor directly into your debt-to-income ratio for your loan.

The Insurance Reality

Here is the big one that catches out-of-towners off guard: Fire Insurance. If you are looking at homes in the San Lorenzo Valley (like Felton or Boulder Creek) or the Aptos Hills, obtaining standard insurance can be difficult. You may be required to get coverage through the California FAIR plan, which is significantly more expensive than a standard policy. This can add hundreds of dollars to your monthly payment, so you must investigate insurance quotes before you fall in love with a cabin in the redwoods.

Lastly, if you are targeting those entry-level condos or townhomes, don’t forget the HOA fees. These can range widely depending on the amenities (pools, gates, etc.), and they factor directly into your debt-to-income ratio for loan qualification.

Best Neighborhoods for First-Time Buyers

Santa Cruz County is incredibly diverse; a ten-minute drive can take you from a foggy redwood grove to a sunny beach town. For first-time buyers looking for the best balance of lifestyle and affordability, these neighborhoods are the top contenders:

- Watsonville: If you want a single-family home with a yard without the $1.5M price tag, this is your best bet. With a lower price per square foot and a rich agricultural heritage, it offers the best “bang for your buck” in the county.

- Live Oak: Sandwiched between Santa Cruz and Capitola, Live Oak offers “surfside simplicity.” As unincorporated territory, it features a high concentration of condos and townhomes, making it a perfect, centrally located launchpad for first-time owners.

- San Lorenzo Valley (Felton/Ben Lomond): Known for “cabin-core” living, this area offers more land and larger houses for your money. It is beautiful and quiet, though you must weigh the lower sticker price against the Highway 9 commute and higher fire insurance costs.

- Scotts Valley: Ideal for those commuting “over the hill” to Silicon Valley, this area feels more suburban and polished. It is highly sought after for its excellent schools and a solid inventory of turnkey condos.

- Soquel: This village has a charming, small-town vibe with antique shops and local restaurants. The market here is a unique mix of character-filled older homes and modern townhome developments, offering great highway access to the rest of the county.

Navigating the Offer and Closing Process

Getting an offer accepted here is an art form. First and foremost, local expertise matters. Finding the best real estate agent in Santa Cruz can make all the difference, as listing agents trust professionals who know how to handle private roads, septic inspections, and coastal commission rules.

A pre-approval letter from a big box online bank often gets pushed to the bottom of the pile because sellers worry the deal will fall through.

When it comes to the contract, we need to talk about contingencies. These are your safety nets—inspection, loan, and appraisal. In the hottest markets, buyers were waiving these entirely.

Today, you can often keep your inspection contingency, which I highly recommend. You need to know if that charming bungalow has foundation issues. Escrow periods typically run 30 to 45 days, giving you time to do your due diligence, but you need to move efficiently.

FAQs

What is the minimum down payment for a house in Santa Cruz?

You do not need 20% down to buy a home. While 20% avoids mortgage insurance, many first-time buyers use FHA loans (3.5% down) or conventional loans with as little as 3% down. If you qualify for CalHFA or other local programs, your out-of-pocket costs could be even lower.

How do I qualify for a Measure J home?

To buy a Measure J home, you typically need to meet specific income limits (moderate or low income) and household size requirements. Crucially, you must demonstrate that you have lived or worked within Santa Cruz County for at least 60 days before applying. Priority is often given to those who work in the county.

Is it better to buy a condo or a house for my first purchase?

In Santa Cruz, a condo is often the most realistic entry point due to the high price of single-family homes. While houses generally appreciate faster, a condo allows you to lock in your housing costs and build equity sooner. It is often better to buy a condo now than to rent for five more years waiting to afford a house.

Are there special taxes for buying in the City of Santa Cruz?

Yes, the City of Santa Cruz has its own transfer tax regulations and rates that may differ from the unincorporated areas of Santa Cruz County. Additionally, if you are buying a Measure O unit, you are subject to city-specific inclusionary housing rules. Always check the jurisdiction of the property address to know exactly which tax rates apply.

Leave a Reply